Arrestments &

Debt Collection

Transparency

Turning a stressful legal-banking scenario into a clear self-service experience that helps clients understand what happened, what money was affected, and what they can do next.

Key Achievements

−23.8%

Support inquiries, first-time collections (Segment A)

−18.5%

Support inquiries, repeat collections (Segment B)

−31%

Trigger-based inquiries after arrest notifications

−21%

Back-office requests in the test group

~20m ₽

Annual savings from reduced support volume

7%

Inquiries fully resolved by chatbot with new intents

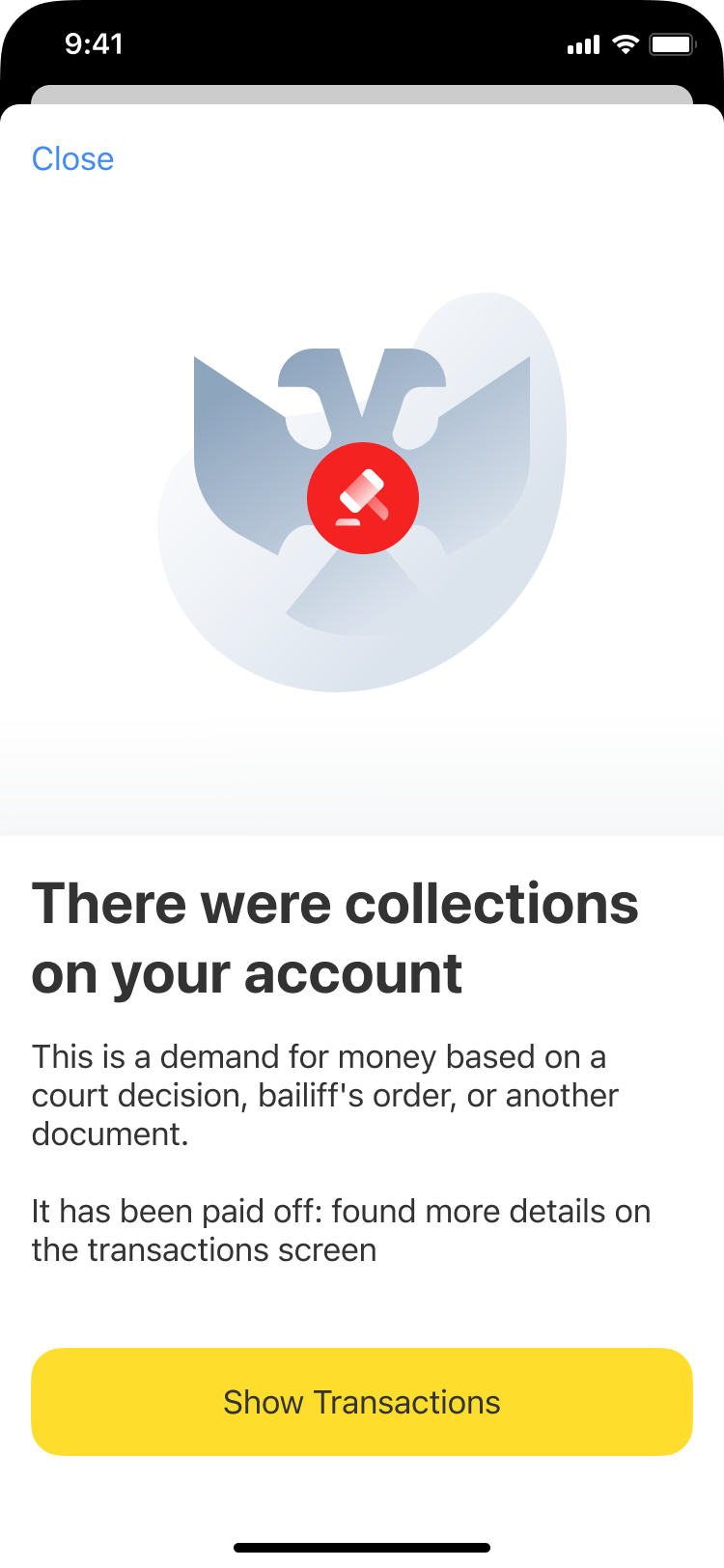

(01) Challenge

A "black box"

at the worst

possible moment

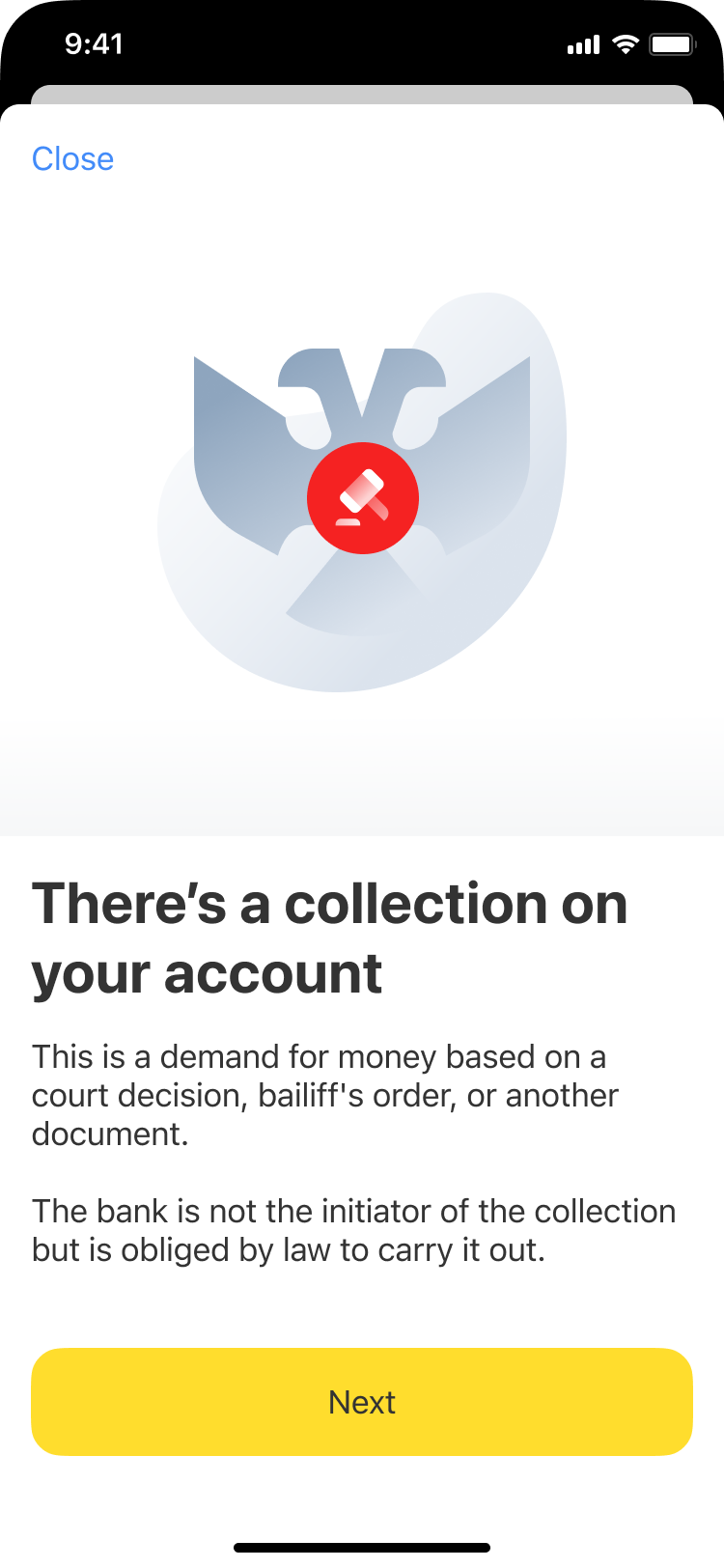

When users fall behind on taxes, traffic fines, utilities, or alimony, bailiffs can issue enforcement orders to freeze bank accounts — often without any prior notice. At T-Bank, with 48M customers, this is a high-frequency, high-stakes event.

The experience was a dead end. Customers would discover the freeze through a failed transaction at checkout, a sudden zero balance, or a cryptic line in their history. There was no clear path to resolution — only confusion, panic, and a call to support.

Goal

Make debt arrests fully transparent — give every user instant clarity

on what happened, why, and the exact steps to resolve it.

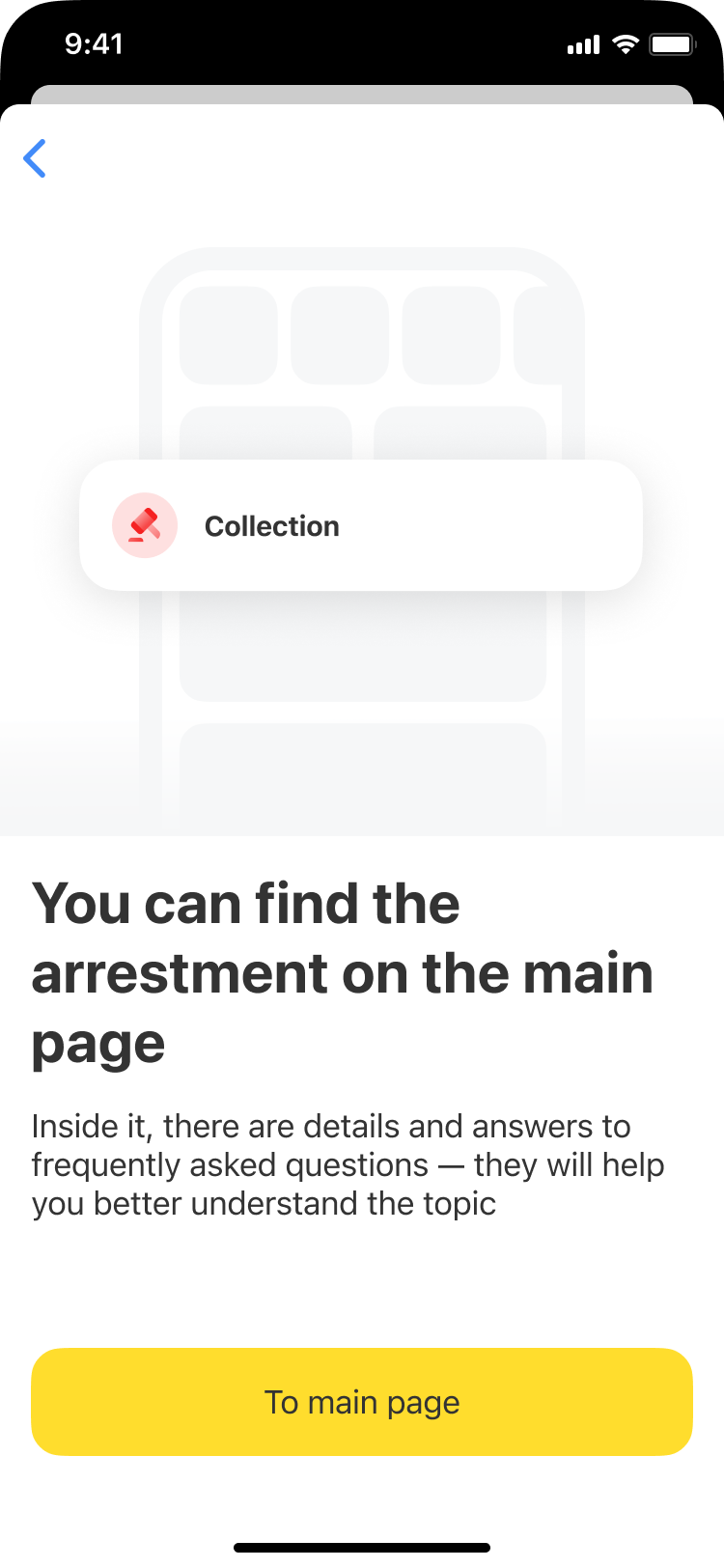

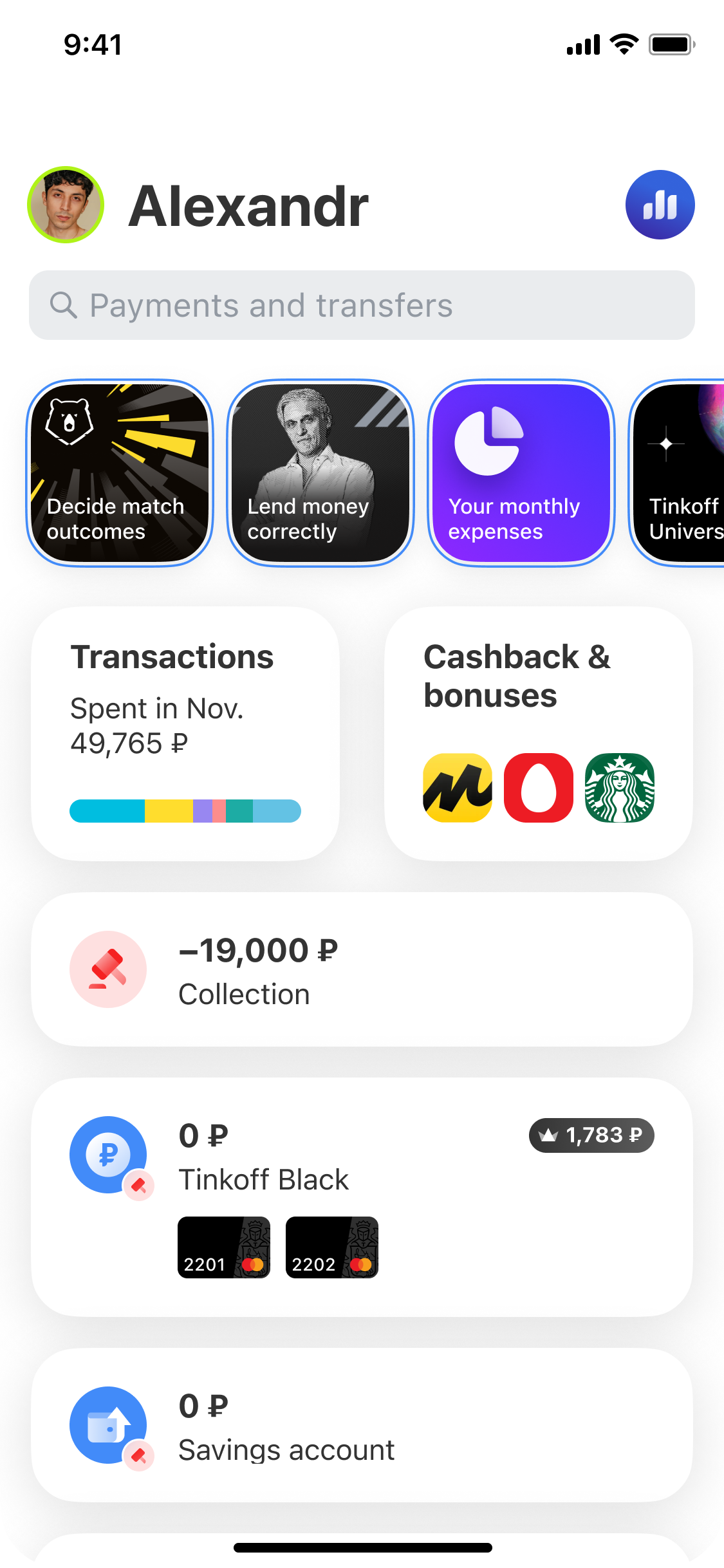

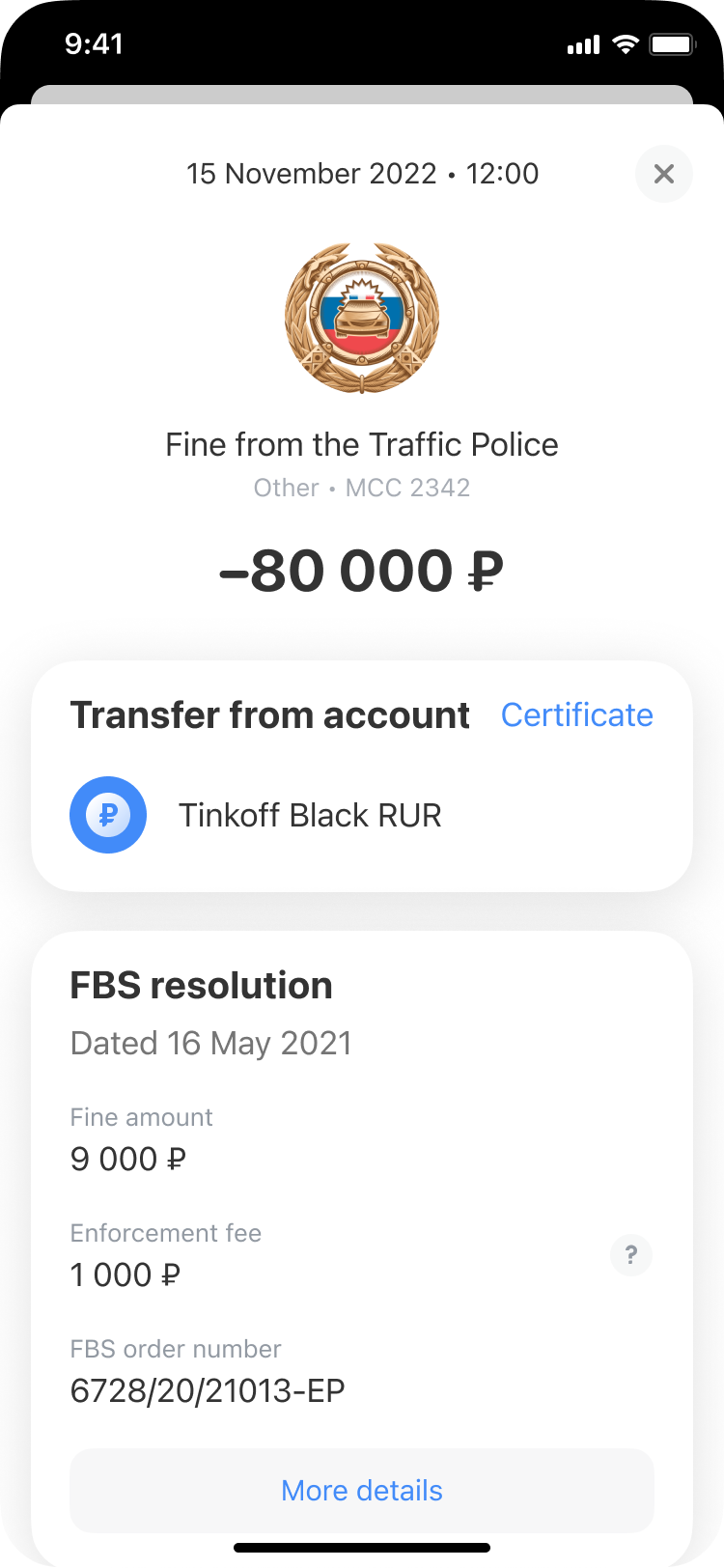

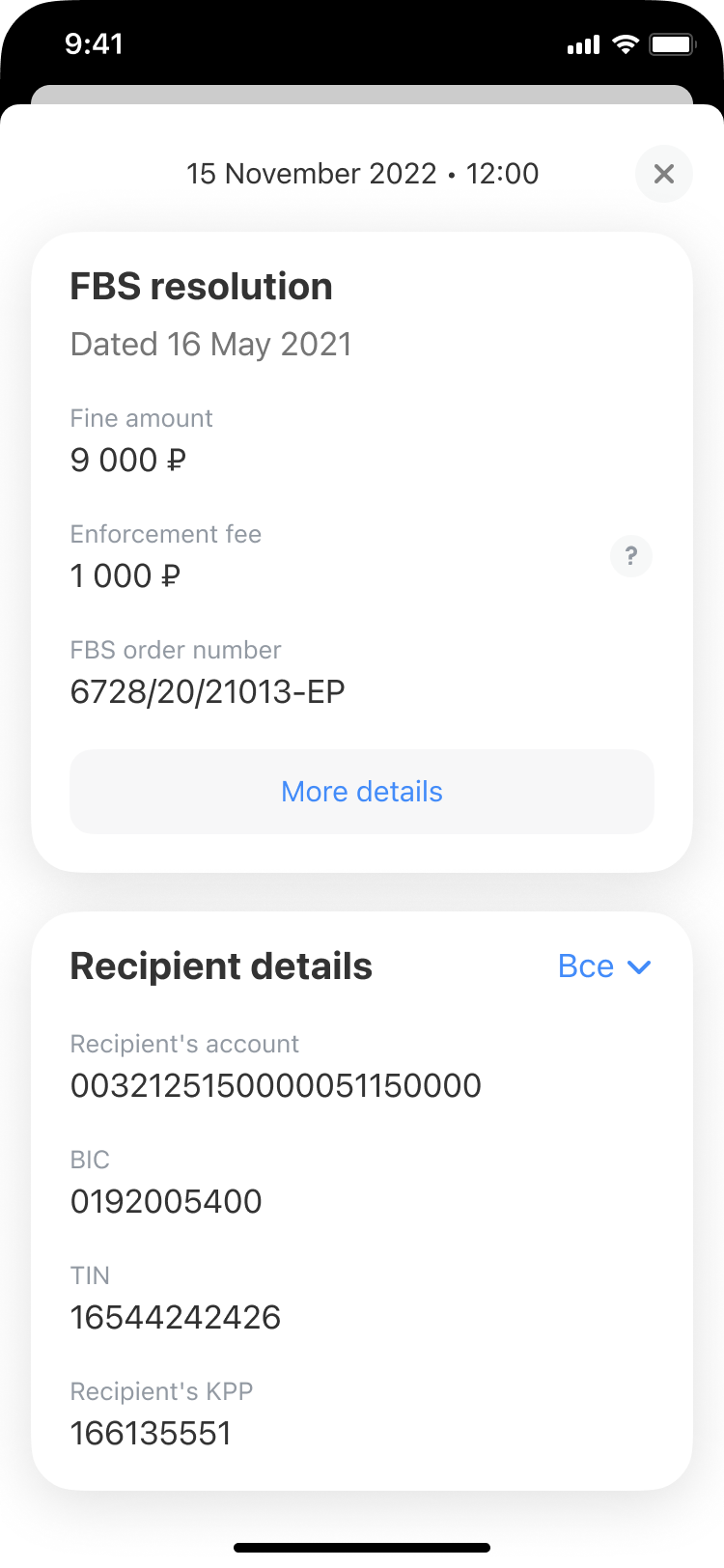

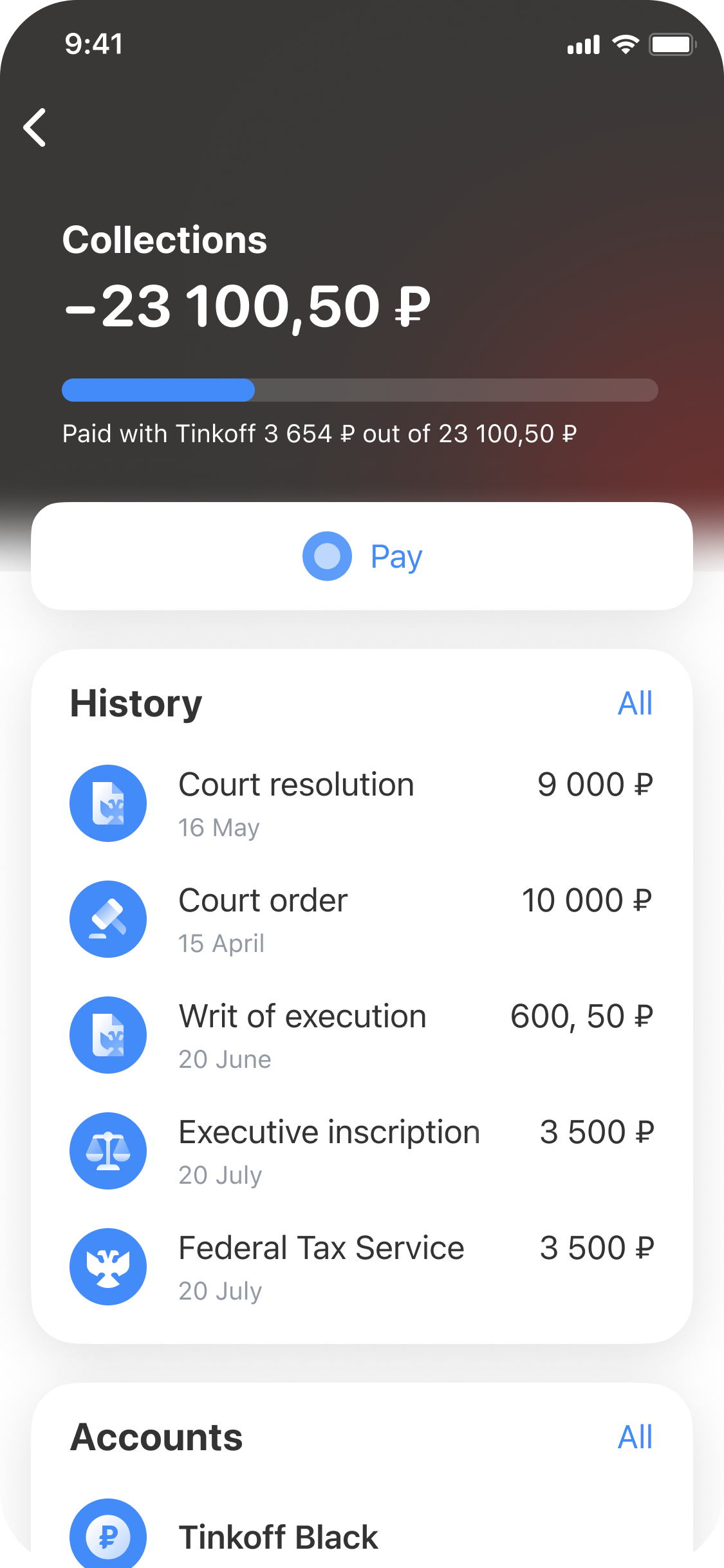

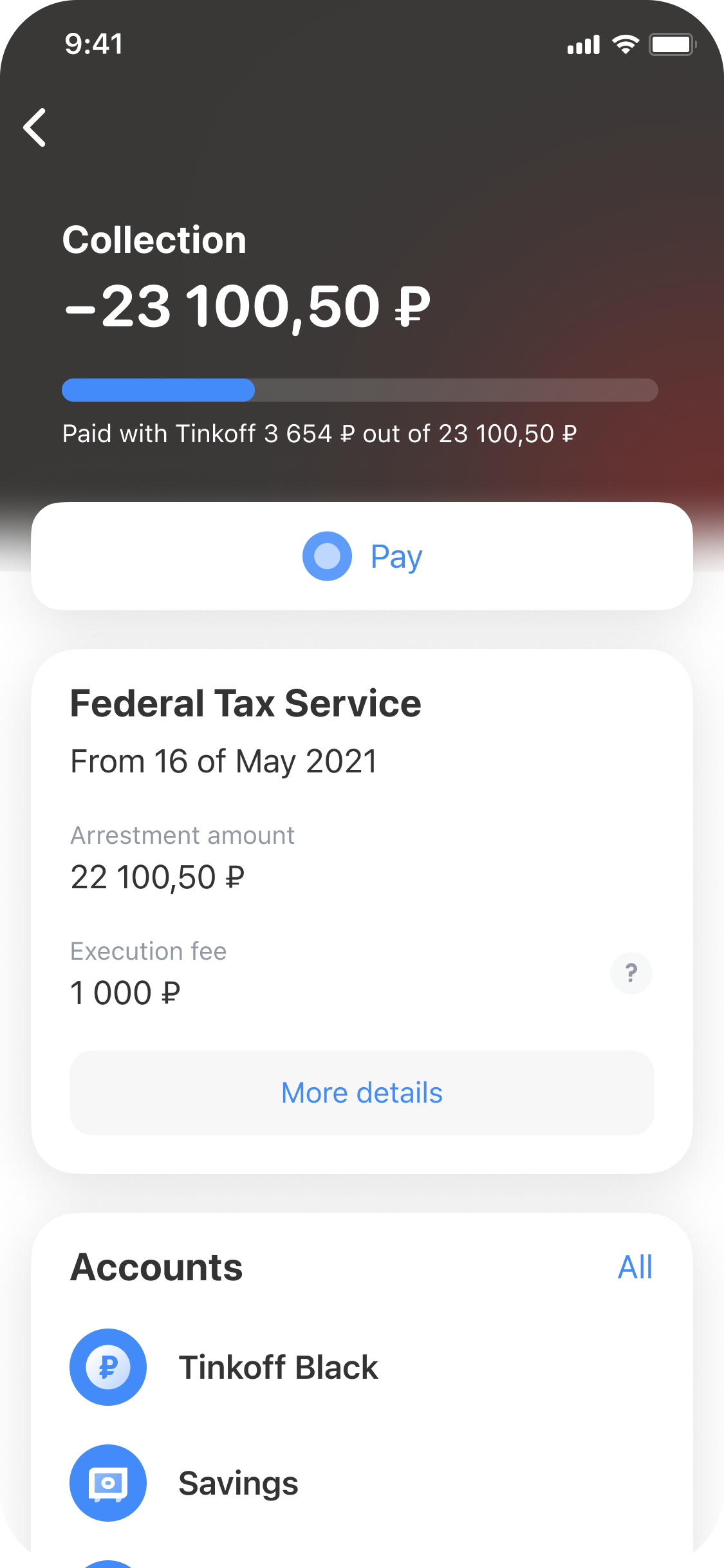

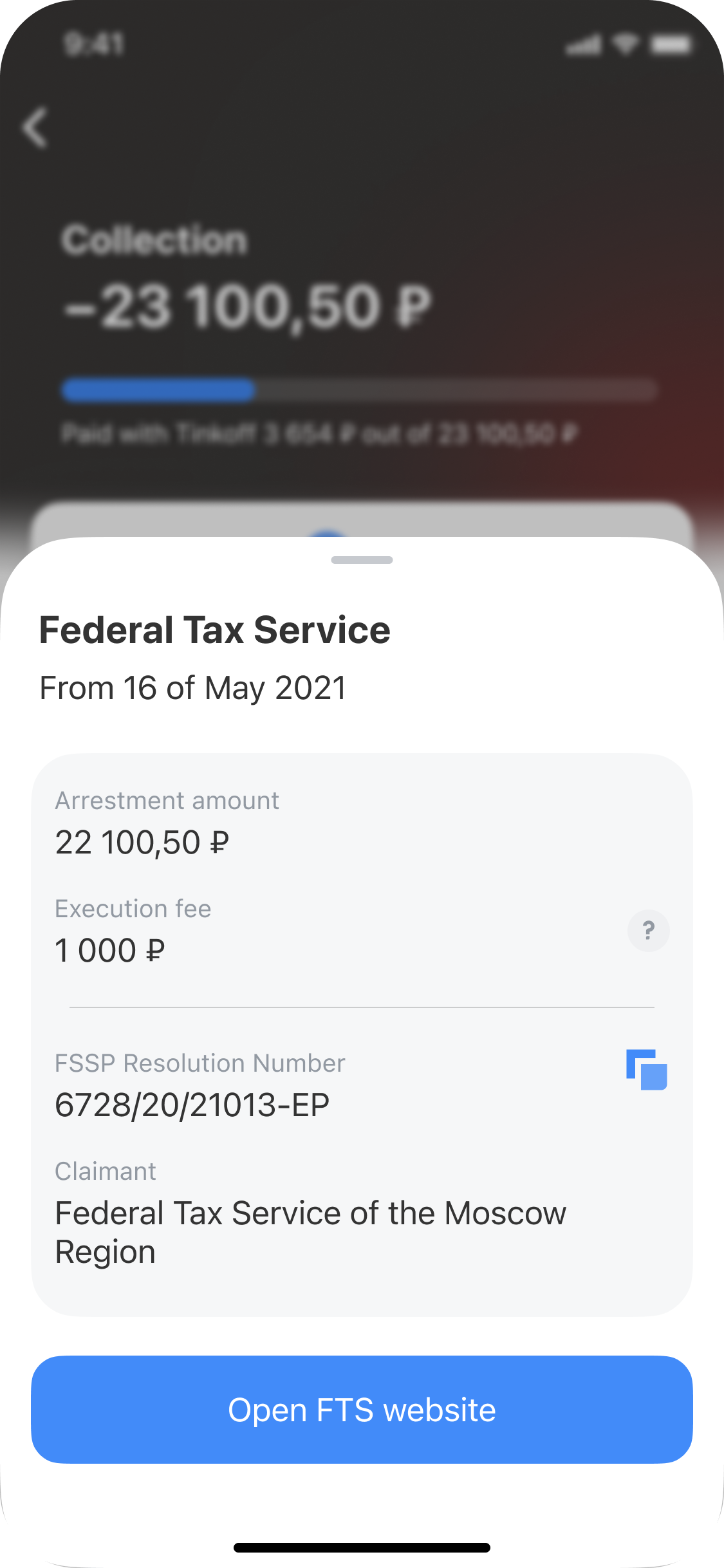

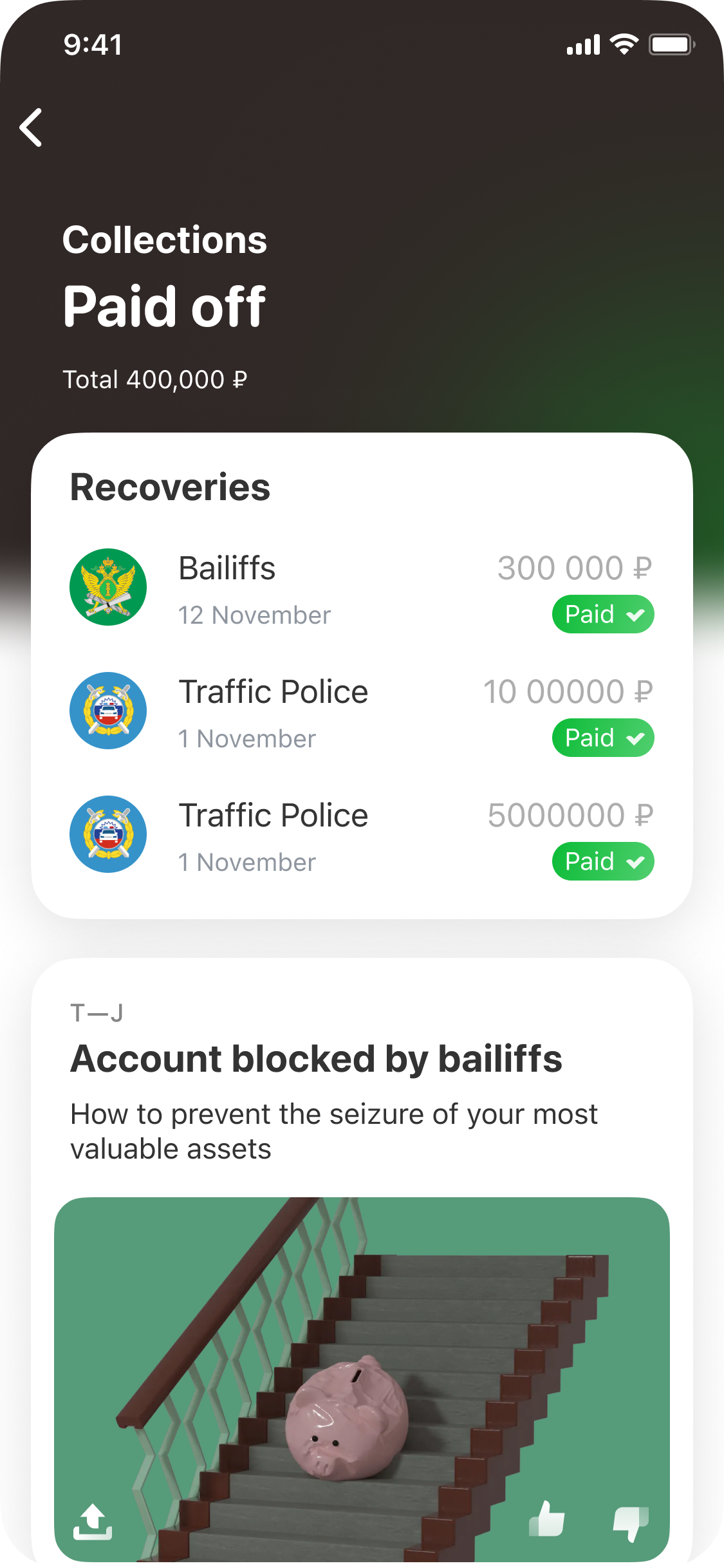

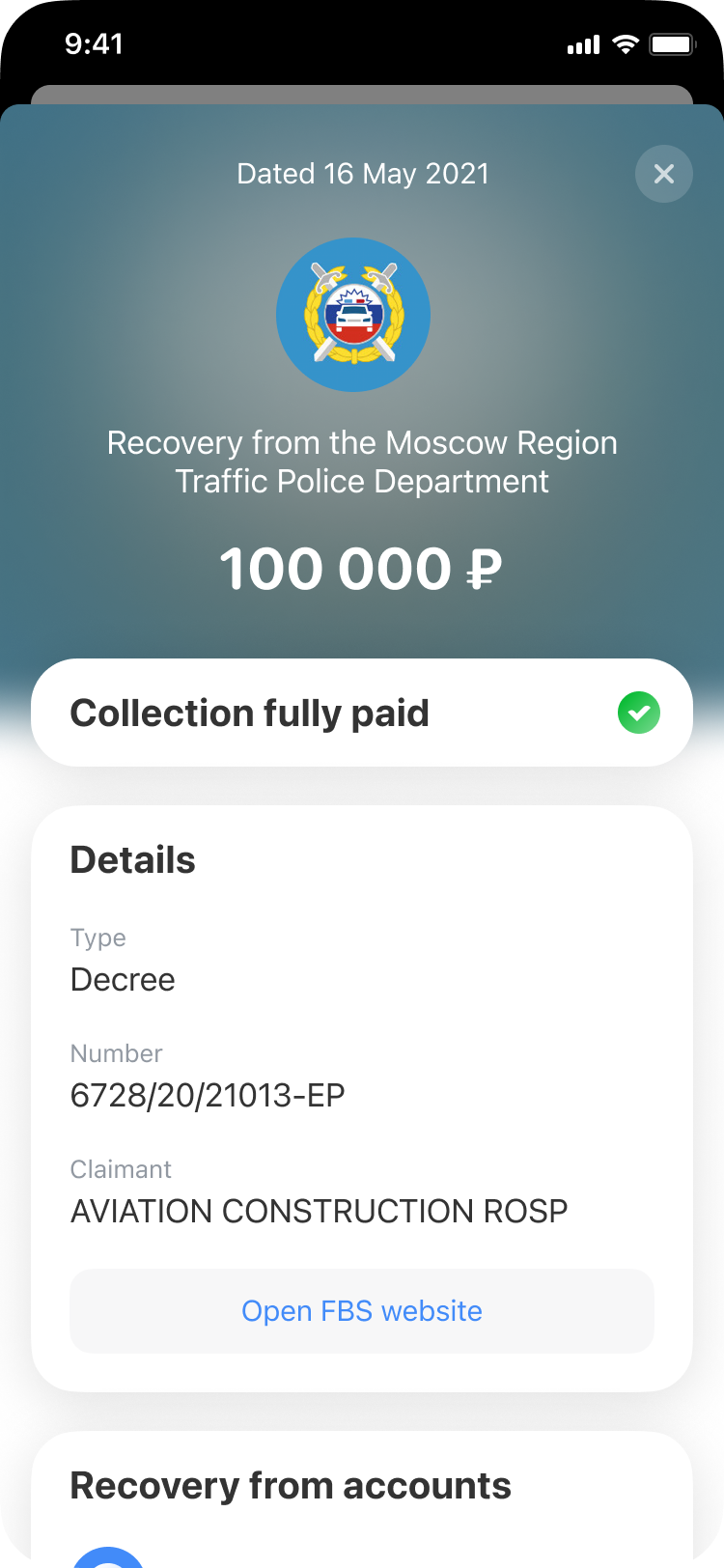

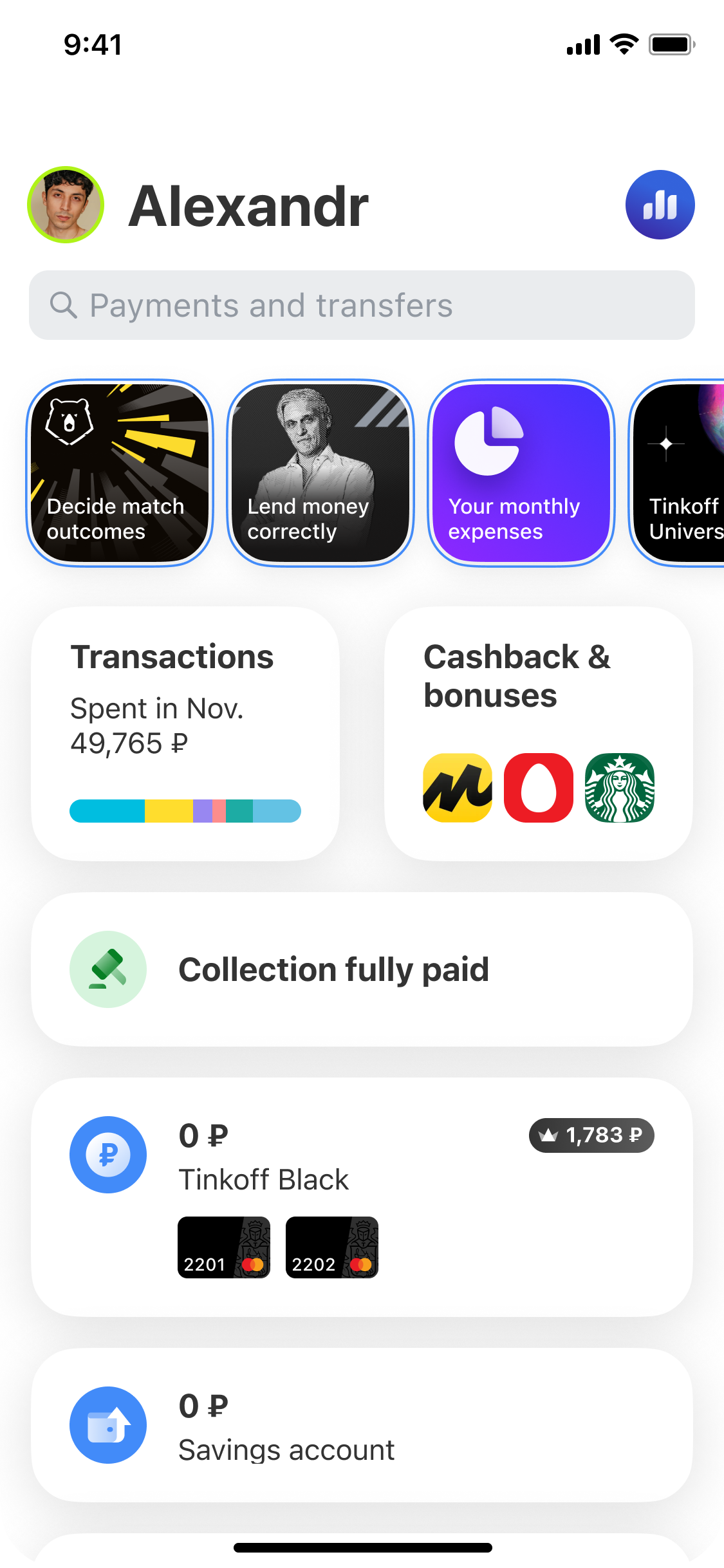

Final flows

The user faced a funds seizure for the first time

Enforcement collection imposed and funds debited

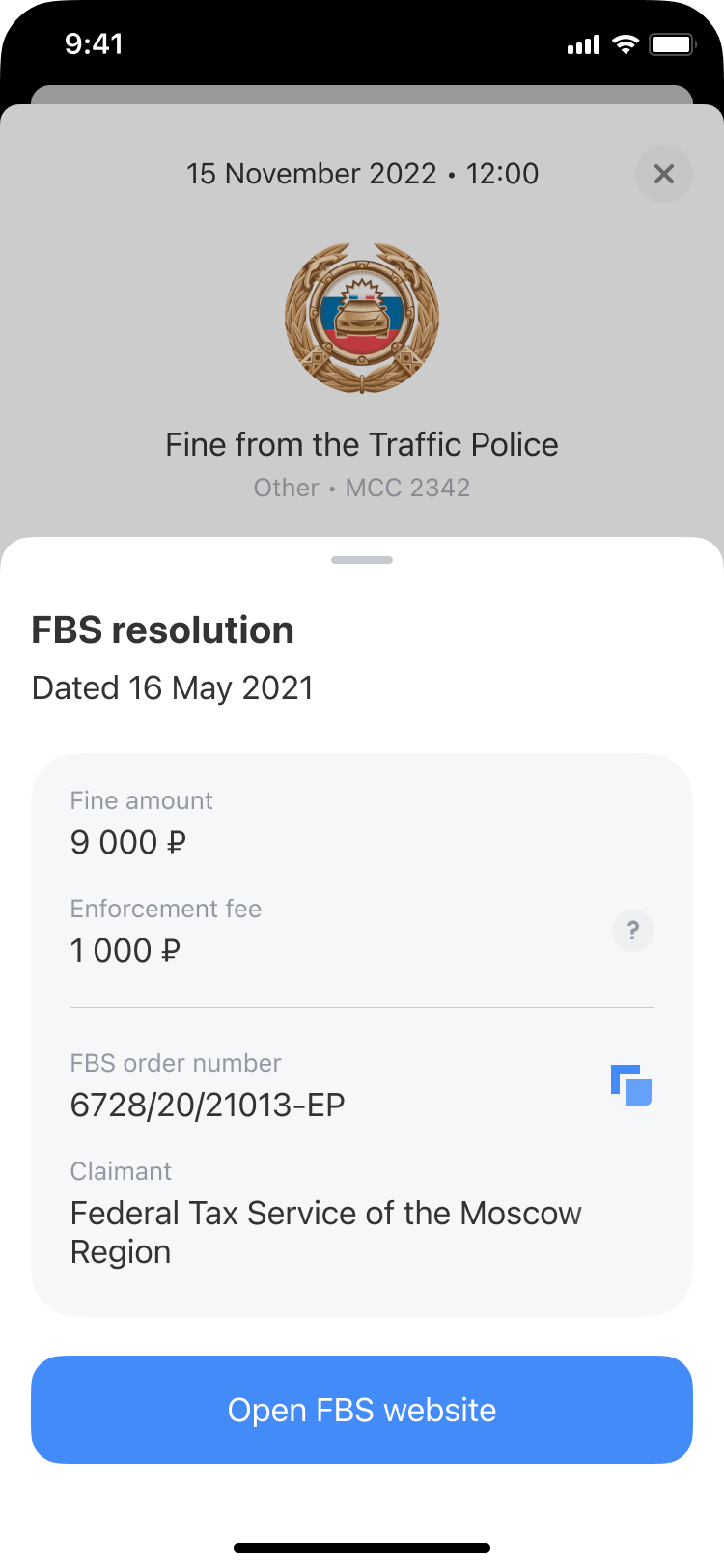

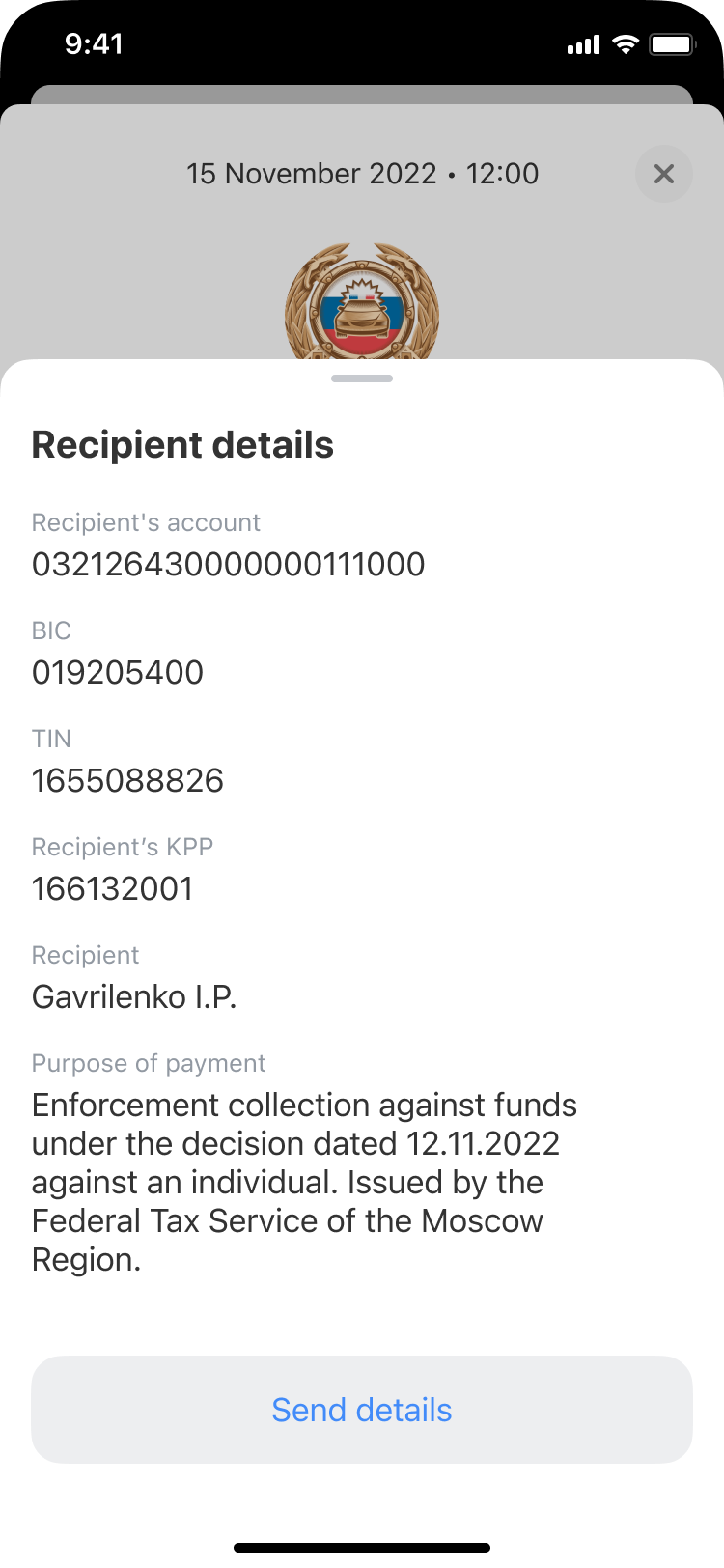

Details

The enforcement collection has been settled

My Role

I joined as the only designer to transform this dead end into a transparent self-service flow. An initial concept existed but was outdated — missing transaction visibility, payment options, and detailed debt information.

Actions

Fixed the data flow

In collaboration with the PM and multiple teams to make sure users could actually see their debt details instead of just a blank screen.

Simplified legal language

Using guidelines from our compliance team, I translated scary legal terms into clear, human-friendly text to reduce user panic.

Built a recovery path

I designed the flow that allowed users to pay off their debts and unfreeze their accounts directly in the app.

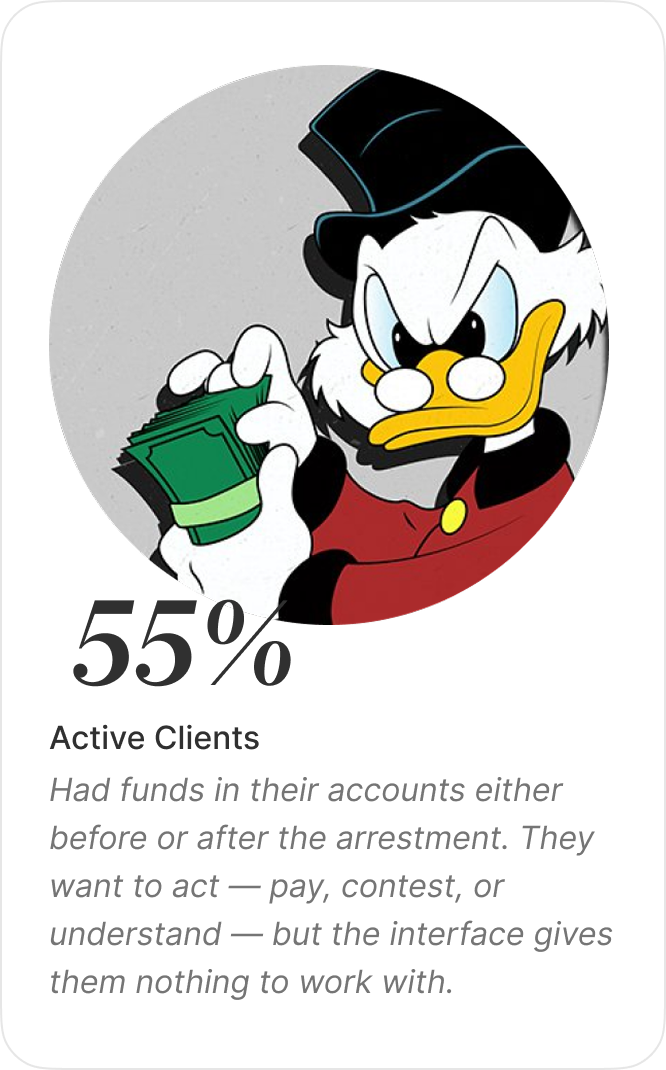

Client profile under debt Collection

CORE PAIN

No visibility into what was taken or what remains accessible

Could resolve instantly, but the interface made it nearly impossible to find how

Feared delinquency but had no way to pay loans while accounts were frozen

Baseline

~ 280k

Monthly orders

142K unique clients affected

250k

Support contacts in the same period

Nearly 1 contact per order. Every arrest triggered a call

80%

Had only one arrest

20% were dealing with multiple simultaneous orders

4%

Resolved within a month

Most took longer than 10 days, a prolonged, stressful experience

~ 50%

Had no funds at the time of arrest

Likely inactive accounts, yet still generating confusion and support load when the order arrived

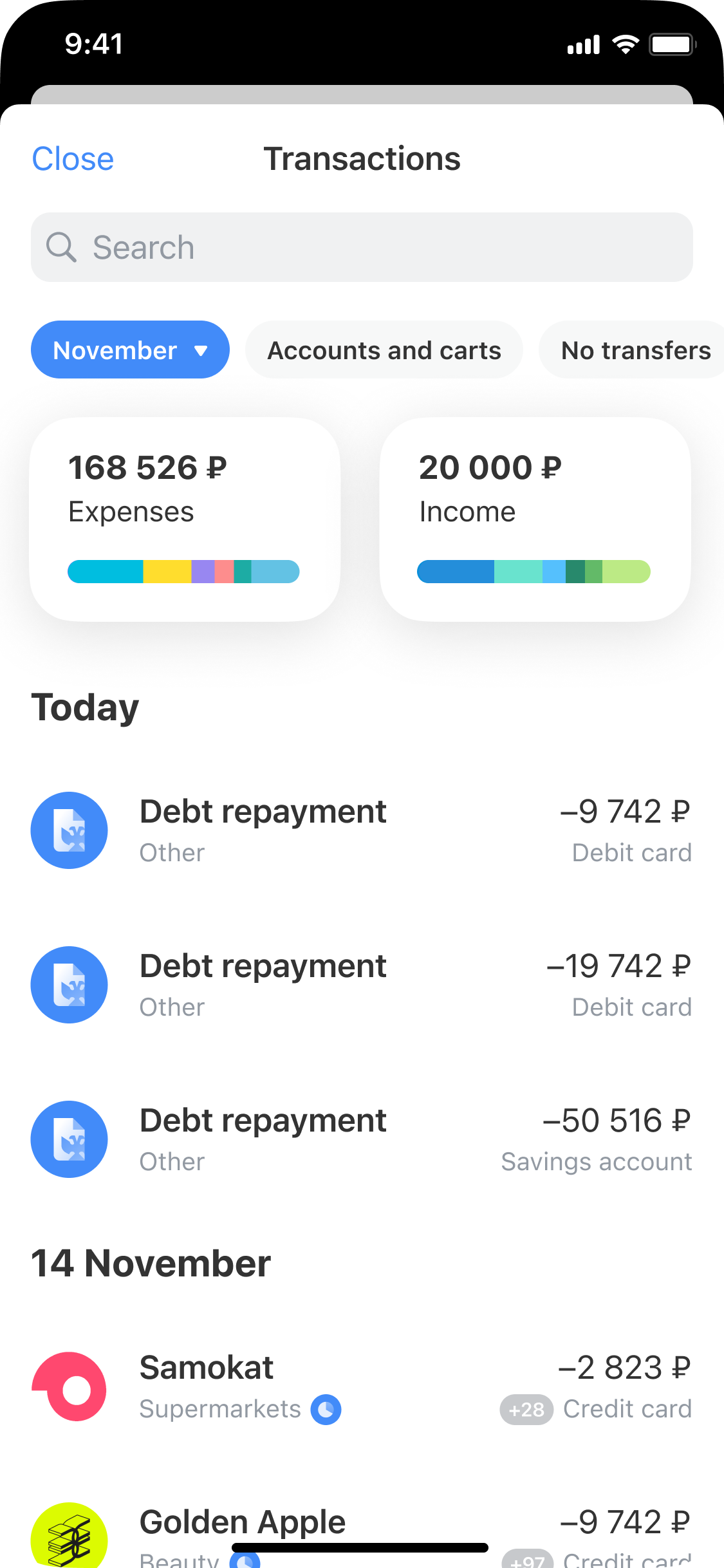

How clients found out about the existing enforcement collection before:

Failed payment attempt

Payment fails

because their accounts have been reduced to

zero or negative balance

.

In the mobile app

When running the app, the client can see a

negative balance

or find details about the

write-off

in the transaction history.

SMS from bank

The bank sends an

SMS

, notifying the client about the start of the collection process.

On the State Services portal (Gosuslugi):

Information about the debt collection might appear on

Gosuslugi

earlier than in the bank's system, allowing the client to learn about it in advance.

(2) Design and Development Process

Data Collection & Approval

I worked with multiple teams to gather real-time collection data and consulted compliance for accurate legal guidance. This provided the foundation for building an interface that would deliver the needed clarity and transparency for customers.

Defining the main problems

USER PROBLEM

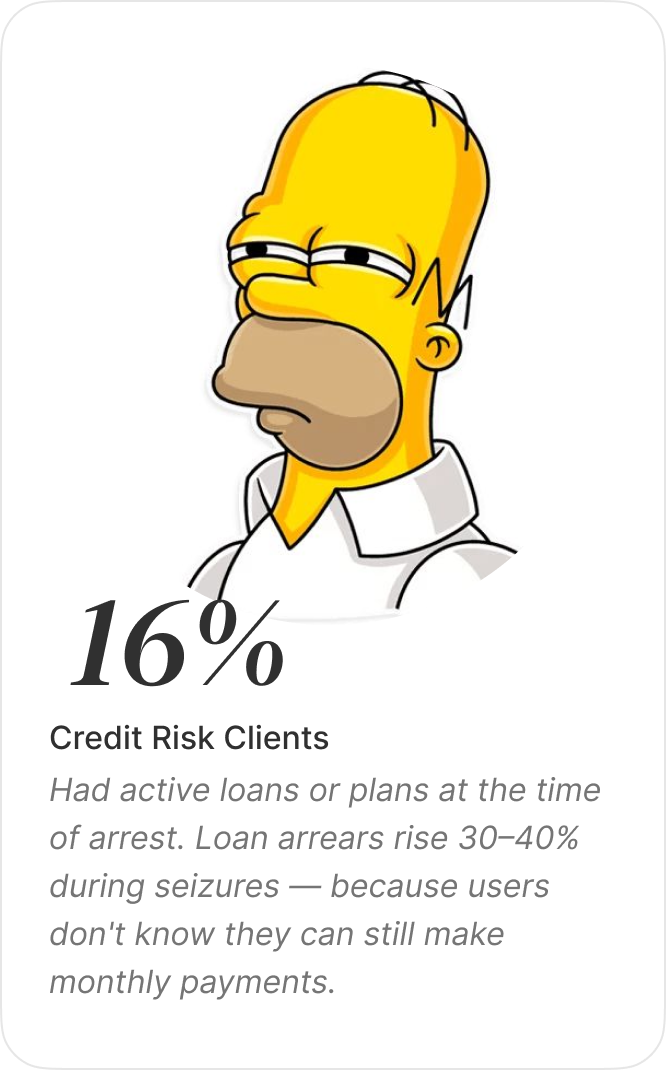

Customers had no way to understand what was arrested, what was accessible, why it happened, or what to do. Loan arrears rose 30 - 40% during seizures because users didn't know they could still pay.

01

No dedicated arrestments screen

02

No transaction visibility for write-offs

03

No explanation of legal context

04

No loan payment path under seizure

BUSINESS PROBLEM

Every enforcement batch triggered a spike in support contacts. Many clients were closing accounts to escape restrictions — a retention problem layered on top of a support problem.

01

High support call and back-office volume

02

No chatbot intents for arrest topics

03

Client churn from account closures

04

Overlapping issues: loans + deposits + piggy bank + payment installments

DESIGN TENSION

Three parties, intersecting flows, legal constraints. The interface had to serve all three — without violating law or sacrificing any side's core interest.

User

Must pay the loan to avoid delinquency — but the seized account blocks standard payment paths. Needs a way out that's visible and accessible.

Bank

Wants to retain the client and prevent loan default — but cannot redirect seized funds to a loan account before the enforcement order is satisfied.

Law

Enforcement order must be settled first. Seized funds cannot flow to another obligation. Every action the interface offers must be legally permissible.

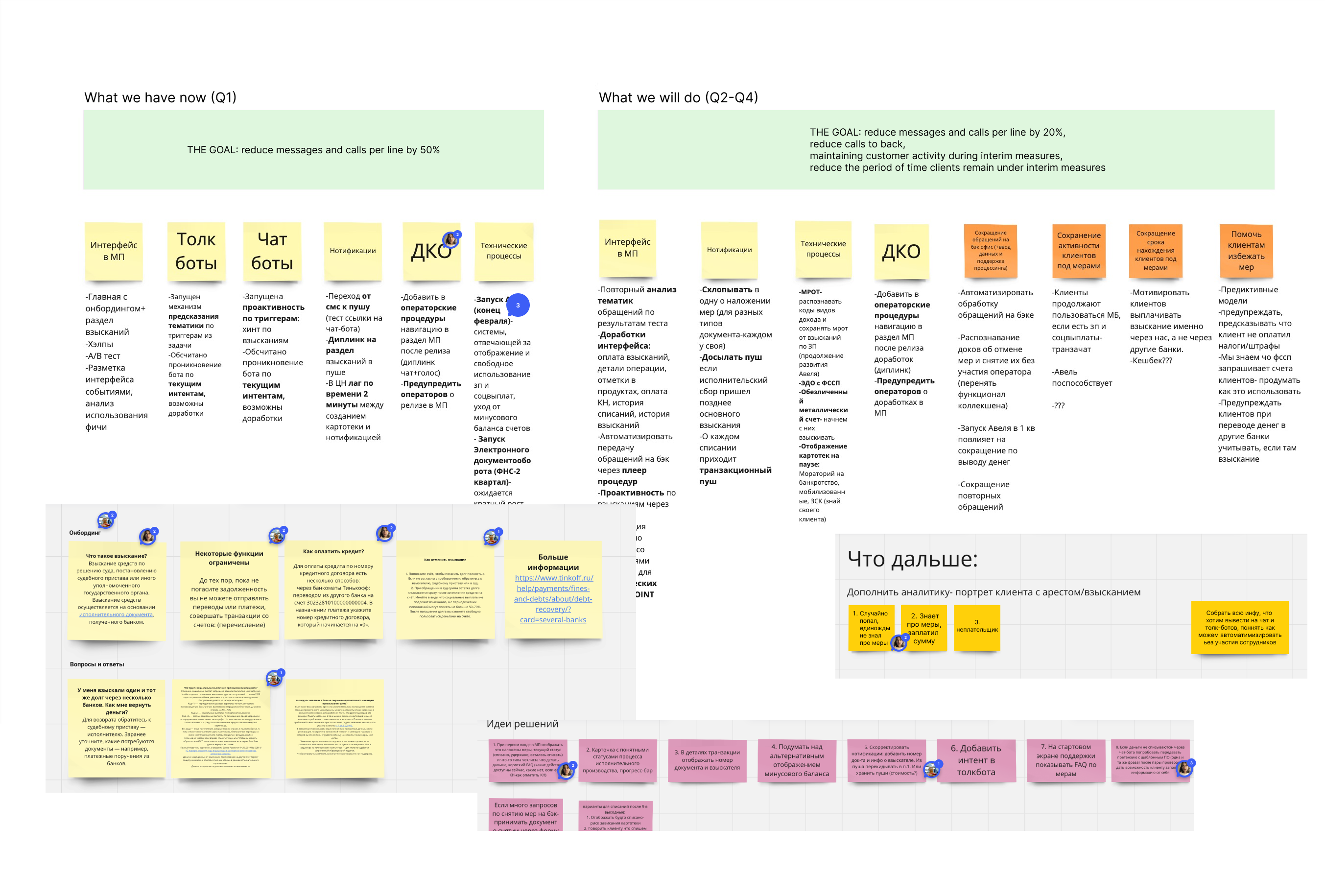

Creating & Testing Interfaces

We developed several user flow options and tested them in two rounds — first with support staff, then with real users. The order mattered: agents knew the questions cold. Their patterns became the product.

Flow exploration

Multiple flow options were developed for key scenarios — arrest discovery, status overview, payment path, loan handling under seizure. Each option made different tradeoffs between legal completeness and cognitive load.

Testing with support agents first

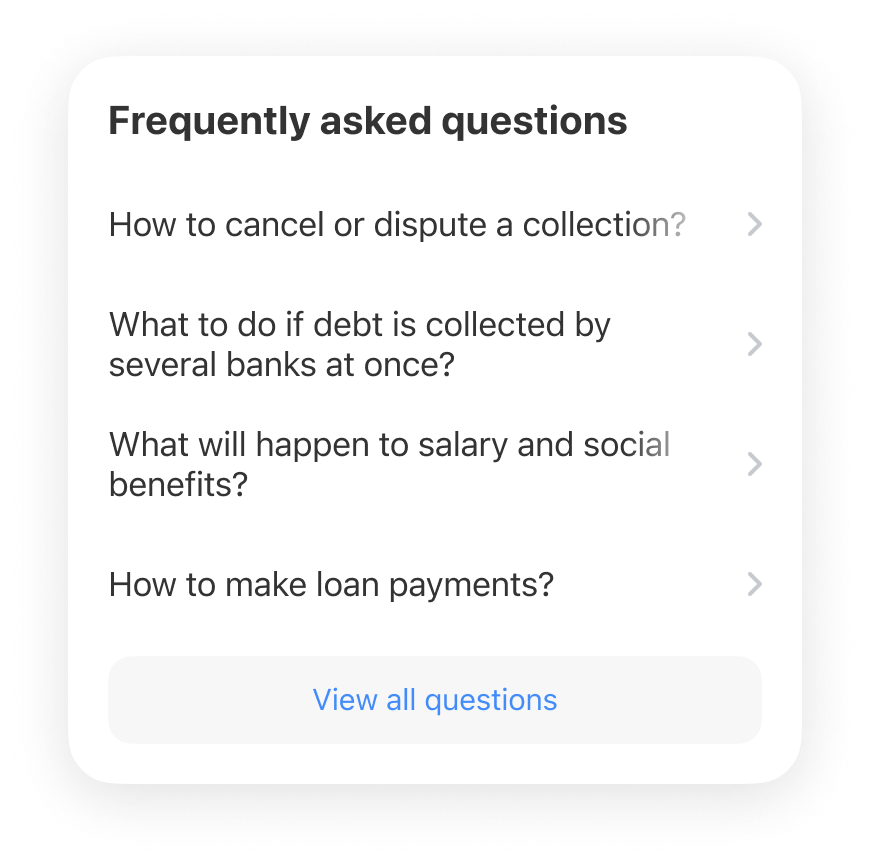

Before exposing flows to real users, we ran sessions with support staff. They had handled thousands of arrest-related calls and knew exactly where panic peaked. Their answers shaped the FAQ section directly.

By testing the concept with support agents, we uncovered the most common customer questions and pain points. These insights became the foundation for the new FAQ section.

Testing with actual users

Flows were then tested across both segments. First-time users needed more explanation and reassurance. Repeat users needed faster access to action. The iteration scope was built from these findings — not assumptions.

(05) Reflection

In sensitive financial scenarios, clarity — is a trust mechanism.

The strongest design decisions were not about adding more information, but about structuring it in the right order: what happened, why it happened, what money was affected, what the client can do now, and then... what happens next.